Fraud Prevention

Overview

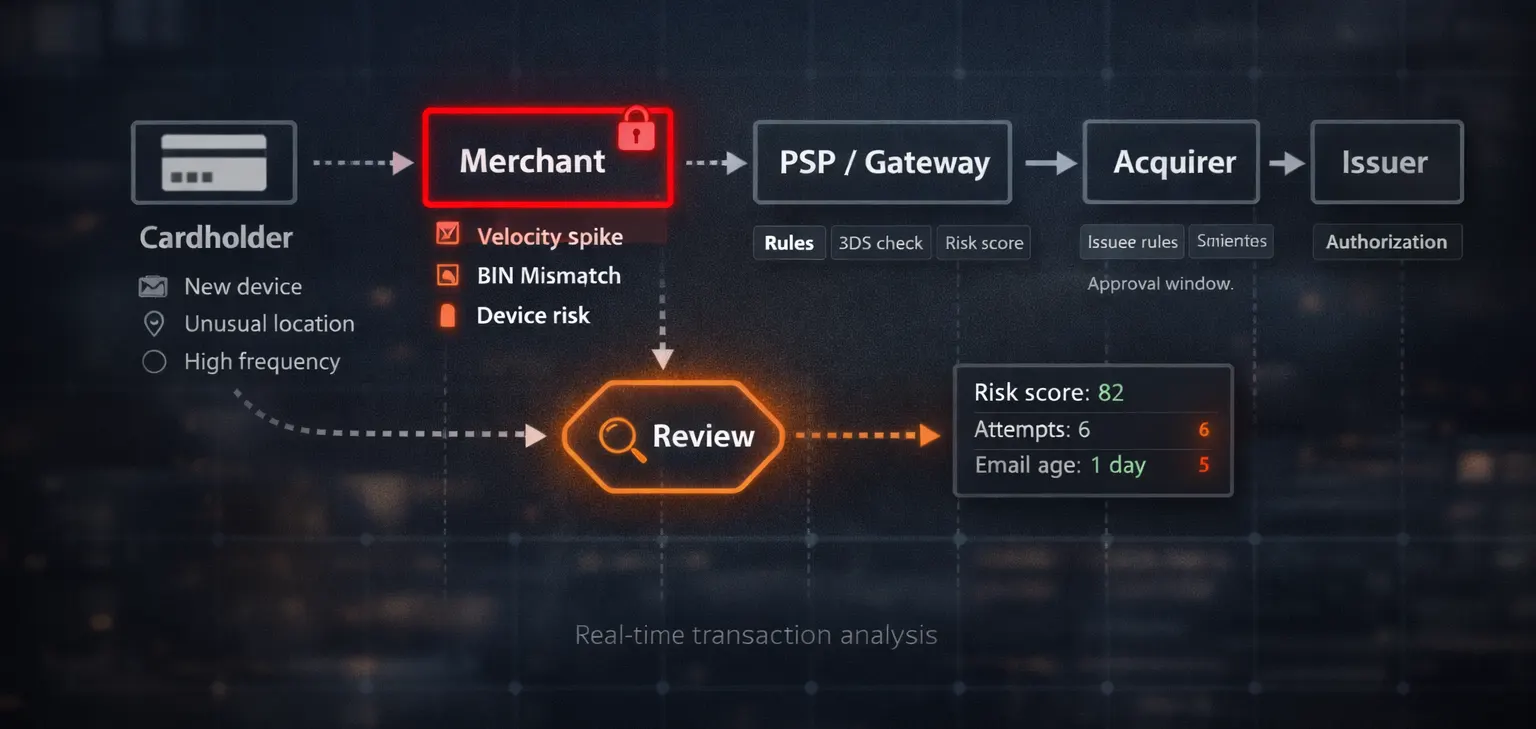

Fraud prevention focuses on limiting unauthorized or abusive activity before it results in financial loss. The work is operational and continuous, tied to transaction flows, user behavior, and platform constraints. Controls are applied with the goal of reducing exposure without disrupting normal activity.

Types of Fraud Encountered

Fraud can take different forms depending on the platform model. This may include unauthorized card use, account takeover, promotion abuse, or friendly fraud. Each type requires a different response and level of review.

Transaction Review and Controls

Transactions are reviewed using predefined rules and risk signals. These rules are based on payment data, account activity, and historical patterns. Actions can range from approval to manual review or rejection, depending on risk level.

User Behavior and Account Signals

Fraud prevention is not limited to payments. Account behavior, login activity, and usage patterns are also reviewed. Inconsistent or abnormal behavior is often an early indicator of future issues.

Manual Review Processes

When automated controls are not sufficient, cases are reviewed manually. Reviewers rely on context rather than single indicators. Decisions are documented to ensure consistency and allow later analysis.

Rule Adjustment and Ongoing Tuning

Fraud patterns change over time. Rules and thresholds are reviewed regularly based on outcomes and observed trends. Adjustments are made incrementally to avoid overblocking or increased false positives.

Impact on Disputes and Payments

Effective fraud prevention has a direct impact on dispute levels and payment stability. Reducing fraudulent transactions upstream helps limit chargebacks and account restrictions later. This connection is reviewed as part of normal operations.

Fraud prevention is closely linked to transaction monitoring, where ongoing activity review helps detect patterns that automated controls alone may miss.

Closing Note

Fraud prevention is not a fixed setup. It evolves with transaction volumes, user behavior, and external conditions. Operational discipline and regular review are key to maintaining control over time.